Skip to content

Home

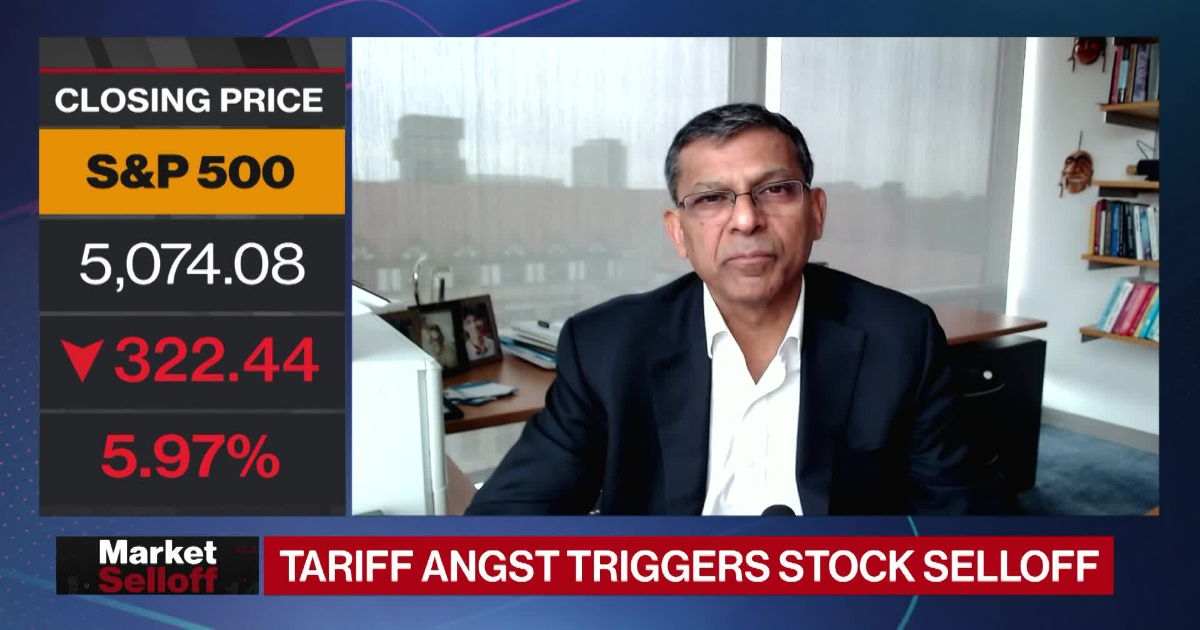

Recession Odds Flirting With 50%, Raghuram Rajan Says

CC-Transcript

- 00:00What is your base case? Is it a recession and a global recession at that, or is it something less? Well, I think the probabilities are flirting with 50% right now of a recession. Think of tariffs as thinking for every percentage point increase in tariffs. A rule of thumb is you get point one percentage points of growth rate. So we were, you know, in a 2% growth economy, maybe two and a half, and you’re taking off 2% of that with a 20% increase in tariffs. So really, we are talking about 020. 5% growth given the tariff increases that have taken place. Of course, as we’ve discussed, you know, there may be some drawback on those tariffs as negotiations take place. And similarly, on inflation, you have to add another two percentage points to inflation because the rule of thumb is point 1% increase in inflation is you have one percentage point increase in tariffs. So we’re talking about, you know, four and a half to 5% inflation by the end of the year. So all this means the Fed can’t really come in on this. Growth plummets. And and we are going to see some shrinkage in growth. I think the one, one and a half percent that investment banks were talking about before the announcement of the tariffs has gone much bleaker at this point. I think back to what President Trump said today, which is my policies will never change. He also urged Jay Powell to cut interest rates, saying it’s the perfect time for that. Do you think Powell is in danger of being demoted from Fed chair? And if so, is there some kind of Fed put as a result? I think it would be a tremendous blow to financial markets if the Fed chairman is removed. All credibility associated with the Fed would vanish in a moment. A lot of people are still confident that the Fed is going to continue as is. Chairman Powell is protected and he will take the right policies going forward if he is removed. I think there will be a lot more panic on financial markets. I hope that doesn’t happen. When you look to this administration, I am curious as to who you look to as being sort of the guiding light when it comes to economic policy and for that matter, maybe the potential for some sort of, I guess, rescue, for lack of a better word, from where we’re at right now? Well, I think this administration is run by essentially one person. It’s President Trump. And unfortunately, you know, whatever advice he’s getting is is reaffirming his natural instincts, which a lot of people have commented on right from the 1980s, that he believes tariffs are, in fact, good and that in the medium term it will create a lot more jobs domestically. I think most economists, including me, are skeptical about them creating jobs in the medium term. But we are almost sure that in the short term there’s going to be a lot of pain. I think Gregory Mangcu from Harvard University said it right. He was the chief economic chairman of the Council of Economic Advisers to President Bush. He said it’s short term pain in order to get long term pain. Is that is there a sense, though, that at this stage that I guess long term gain can actually be done? And I ask because we had on Bloomberg Television a little bit earlier, the head of the Council of Economic Advisers was kind of making this case, look that once you get to, you know, the budget process and tax cuts and some of these other proposals that are out there, that somehow that ends up becoming the sell, that that provides enough juice for the economy to blunt, if not a, erase the negative impact from tariffs. You’re an economist. Is that how it works? I mean, certainly some deregulation, some lower taxes for businesses can help elevate spirits. But tariffs of this kind, this is, remember, the highest level since 1909. They do a lot of damage to the existing supply chains. We’ve had global supply chains like never before, and those are going to be interrupted. The belief is somehow that we will get jobs back into the United States over time. But think about what kinds of jobs are going to come back to the United States. The jobs where you don’t need much labor because labor is costly in the United States. So we are talking about much more capital intensive production. That’s not what the administration wants. It wants more jobs for high school educated people, for moderately educated people, because those are in in their in their support base. That’s not going to happen. So I’m not sure what we’re talking about when we’re talking about medium to long term gain. We have disrupted a situation where we had one of the strongest U.S. economies relative to other industrial economies in in memory. The US came out of the pandemic much better than everybody else. Yeah. And now with 4% unemployment, we’re trying an economic experiment. To do what? To get less unemployment than 4%. That’s hard. Well, you referred to that U.S. exceptionalism. I think about Howard Marks of Oaktree, who was on Bloomberg Television earlier program. And he was saying that the US has long been a place for global investors who are seeking reliable returns. They want predictable outcomes. They want a strong rule of law. To what extent do they still have that in the US or are both of those diminishing? Well, I think there’s been a lot of uncertainty about policy created recently and that’s why I said if you if you mess with the Fed, that makes it even less, even more uncertain for global investors because that brings inflation into play in a much bigger way than if you left the Fed alone. But I think the there is worry across the board. You know, some of the people in the administration are saying, well, that may play in our favour because we’ll get less investment, financial investment into the United States. The dollar will depreciate, allowing the US to export more. But it comes at a serious cost because you didn’t diminish the attractiveness of US securities. And remember, the US is running a large fiscal deficit which needs all the funding it can get from across the world. I do want to get your thoughts for we leave, Professor, about the New World order, if you will, if that is indeed where we are or where we’re going. There’s been a lot of talk about the lack of influence that the US is sort of putting itself in a position in the idea that there is trust is being eroded and that countries, whether it’s our North American partners or our European partners, are going to seek out maybe a little bit more stability. I don’t know from who. I don’t know if that becomes China or someone else. But do you see that really unfolding or is the dominance of this US economy and the clout that the United States has had basically going back to the 1940s? Is that going to be enough to maybe be the magnet that brings everyone back? Well, it can still carry on for some time. The US is, as you said, the biggest economy. It’s been the most favored economy in terms of capital inflows, etc.. That will continue because it’s not obvious there are alternative places so readily available. But I think the search for alternatives is on, and once the search is on, people will find alternatives, perhaps in regional groupings, Maybe around China, though I suspect the automatic rush to China is not going to happen. It’s got to be more a measured. Okay. We we we find it hard to trade with the US. Who else can we trade with? And so, you know, a country like India is going to look to ASEAN. It’s going to look to Japan. It may even mend its relationships with China and look to trade war with China so that every country is thinking in this way at this point. Yeah. And of course, the US is still big and strong, but it is eroding it.